8 Steps to Start a Business as a Teenager

If you've already got a business idea but aren't sure how to actually turn it into something real, you're not alone. A Junior Achievement USA and The Hartford survey found that 60% of teens would rather start their own business than work a traditional job, and 69% already have an idea, but they just don't know how to start the process. Wanting to start a business as a teenager is common. Knowing the actual sequence, problem, plan, legal basics, and first customer is the part that usually gets skipped.

That's what this blog walks you through: the same process adults use to launch a small business, adapted for your situation specifically, limited time around school, limited capital, and a parent or guardian who needs to be looped in on anything official. Follow it in order, and you finish with a business that's actually operating, not just an idea you've been talking about for months.

Key Takeaways

Starting a business as a teenager works the same way it does for adults: problem, validation, plan, structure, money, and customers, just adapted for your schedule and legal status as a minor.

A one-page business plan is enough to start. You don't need forty pages to test whether an idea works.

Most states require a parent or guardian to be involved in contracts, bank accounts, and business registration for anyone under eighteen.

Track business money separately from your own money from day one, even if the business is small and informal at first.

Testing your idea with real potential customers before you build anything saves you from spending months on something nobody wants.

Mentorship and structure, not just motivation, are usually what turn a school project into a business that keeps running, which is exactly what Young Founders Lab is built to provide, pairing high school founders with mentors who've built their own companies and running hands-on pitch training.

8 Steps to Start a Successful Business as a Teenager in 2026

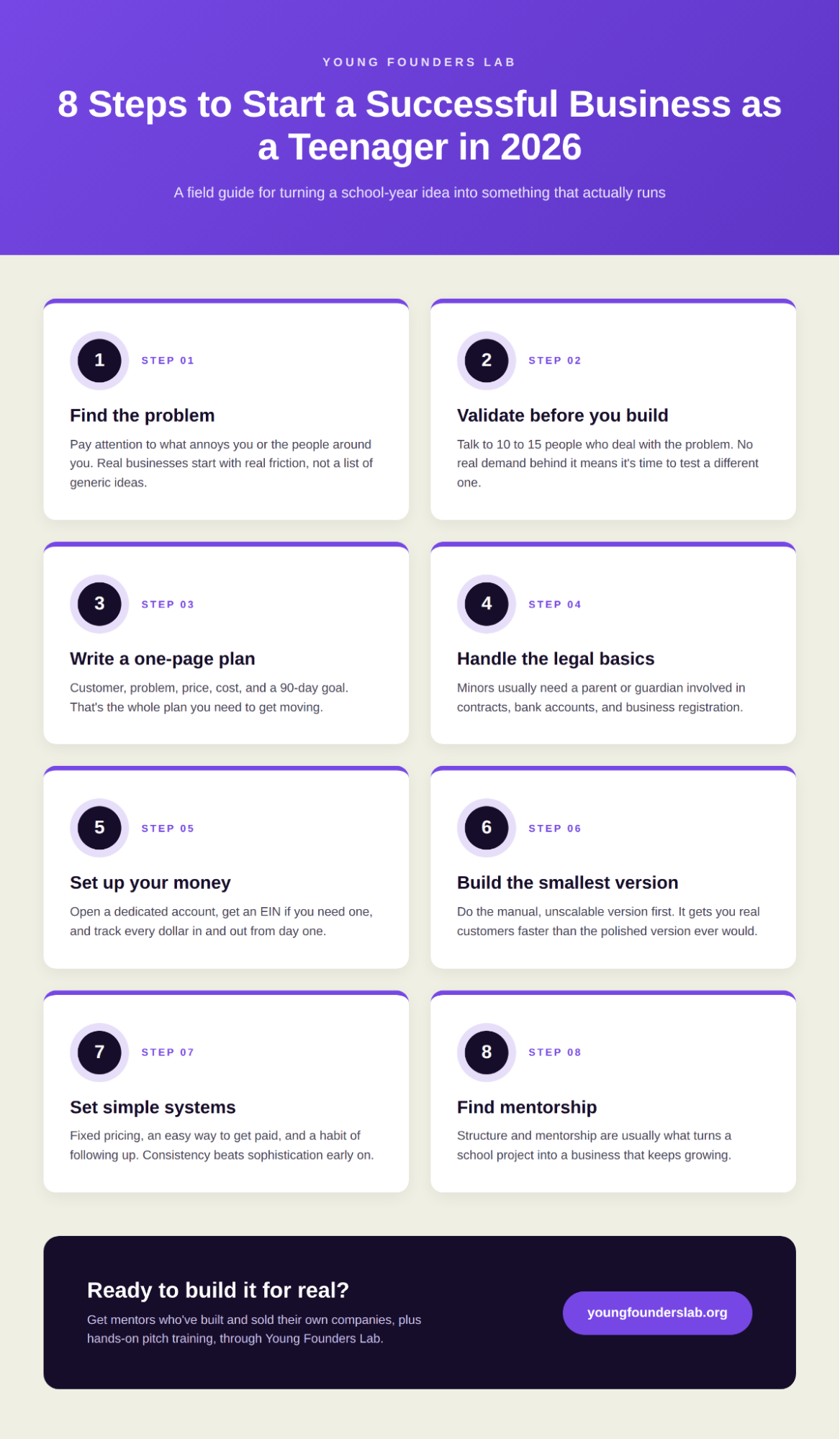

Step 1: Start with a problem you actually care about

Every business starts as a reaction to friction somewhere: a task that takes too long, a service that doesn't exist for people your age, a gap between what's available and what you or your friends actually need. Paul Graham's essay on generating startup ideas makes the case that the most reliable ideas come from problems you've actually experienced, not ones you tried to invent from scratch.

If you already have an idea, skip ahead. If you're still deciding what to build, spend a week paying attention to what annoys you or the people around you and write it down every time it happens, no matter how small. Patterns will show up, and one of them is usually where a real business starts.

Step 2: Validate the idea before you spend any time or money

Once you have a problem worth solving, talk to ten to fifteen people who deal with it before building anything. Ask how they currently handle the problem, what they've tried, and whether they'd actually pay for something better.

CB Insights' research into why startups fail found that 43 percent of shut-down startups it studied cited a lack of real market need, building something people didn't actually want, as a primary cause. That applies just as much to a school project turned business as it does to a funded startup. If people shrug when you describe the problem, that's useful information. It means you should test a different idea rather than force one that has no real demand behind it.

Step 3: Write a one-page business plan

A business plan for your first business as a student doesn't need to be forty pages or full of financial projections you can't back up. One page is enough, and it should answer five questions plainly: who is the customer, what problem are you solving for them, what will you charge, what will it cost you to deliver, and what does success look like in the first three months. SCORE's simple business plan framework is built around this same structure, and it works just as well scaled down for a small, part-time business as it does for a full startup. Keep it short enough that you'll actually look at it again in a month.

Step 4: Handle the legal basics that apply to you as a minor

This is the step most guides skip, and it's the one that trips people up. In most states, anyone under eighteen can't sign a legally binding contract, open a business bank account, or officially register a business entity without a parent or guardian involved. That doesn't mean you can't start a business as a teenager; it means your parent or guardian needs to be part of the paperwork, either as a co-owner, a cosigner, or the person whose name is technically on certain accounts. The Small Business Administration's guide to choosing a business structure walks through the common options:

Sole proprietorship: the simplest structure, often run informally under your own name or a "doing business as" name, though a parent may still need to be involved in banking

LLC: offers liability protection and is common for anyone selling a product or service with any real risk attached, though most states require an adult to be involved in forming it

Operating under a parent's existing business or as an authorized user: sometimes the simplest starting point for a very small, low-risk business

Have a real conversation with a parent or guardian early, not after you've already taken money from a customer. Rules vary by state, so check your specific state's requirements for minors starting a business before you register anything.

Step 5: Set up how you'll handle money before you take a single payment

Keep business money separate from your own money from the very first sale, even if the business is small and part-time. That usually means a dedicated bank account, which will likely need a parent or guardian as a joint holder if you're under eighteen.

If you plan to hire anyone, open an account in a name other than your own, or eventually operate as an LLC, you'll likely need an Employer Identification Number. The IRS explains how to apply for one, and the application is free and takes a few minutes online. Track every dollar in and out from day one. It's a habit that's much easier to build early than to retrofit later once the business has any real revenue.

Step 6: Build the smallest version of your product or service

Resist the urge to build the complete, polished version of your idea before you have a single customer. Paul Graham's essay on doing things that don't scale makes a point that applies directly here: many successful founders started by manually doing the thing their business would eventually automate, personally delivering the service, personally recruiting the first users, and personally handling every order.

Do the manual, unscalable version first. It gets you real customers and real feedback faster than building the ideal version ever would, and it tells you what's actually worth automating later. You're also less early than it might feel: an American Express survey covered by Inc. found that one in five Gen Z and millennial founders were still students when they started their business, compared with just three percent of Gen X and Baby Boomer founders.

Step 7: Set simple systems for pricing, sales, and repeat customers

Once a first version of your business is running, put a few basic systems in place so it doesn't rely entirely on you remembering everything. Decide on your pricing and write it down somewhere consistent, rather than quoting a different number to every customer. Use a simple, free tool for invoicing or payments rather than tracking sales in your head. And build a habit of following up with past customers, since repeat business from people who already trust you is almost always easier to win than a brand new customer. Long-term survival is where this starts to matter:

LendingTree's 2025 analysis of BLS data found that 22.1 percent of new businesses close within their first year and 48.6 percent close within five years, and the ones that make it past that mark are usually the ones running on more than one person's memory. None of this needs to be sophisticated. It needs to be consistent enough that the business runs the same way whether you're actively thinking about it or buried in homework that week.

Step 8: Find mentorship and structure to keep growing

A business that's running is a real accomplishment, and it's also usually the point where founders benefit most from outside structure. SCORE-sponsored research has found that small businesses working with a mentor show higher survival rates than the national average. Y Combinator's guidance to early-stage founders consistently comes back to the same idea: talking to people who've done it before, mentors, and other founders, cuts down on the number of expensive mistakes you make figuring things out alone.

Young Founders Lab pairs high school founders with mentors who've built and sold their own businesses, runs hands-on pitch training, and gives you a structured process for taking a business from something you're running solo to something with real direction and growth. If you've made it through the steps above and have a business that's actually operating, YFL is built for exactly this stage: the jump from a project you started on your own to a venture with mentorship, feedback, and a plan behind it.

Frequently Asked Questions

1. What is entrepreneurship in high school?

Entrepreneurship in high school means identifying a real problem and building a small business or venture to solve it while you're still a student, usually part-time and often with a parent or guardian involved in the legal and financial basics. It can range from an informal service you run for neighbors to a registered business with its own bank account and customers. Programs like Young Founders Lab are built specifically to support students through that process with mentorship and structure, rather than leaving you to figure out every legal and practical detail on your own.

2. Do I need my parents' permission to start a business as a teenager?

In most states, yes, at least for anything official. Minors typically can't sign binding contracts, open a business bank account, or register certain business structures without a parent or guardian involved. You can absolutely start doing the work yourself, testing an idea, finding customers, but a parent or guardian will need to be part of the paperwork once money and legal structure are involved.

3. How much money do I need to start a business as a student?

Many student businesses start with very little, sometimes nothing beyond a phone and the materials you already have. The higher cost is usually time, not money. Focus on testing your idea manually and cheaply before spending on anything, and only invest real money once you've confirmed people actually want what you're offering.

4. Can a high schooler legally form an LLC?

It depends on your state, and in most cases, a minor can be a member of an LLC, but a parent or guardian typically needs to be involved in forming it, since minors generally can't sign the required legal documents on their own. Check your specific state's rules, or start as a sole proprietorship with a parent's involvement and consider forming an LLC later, once the business has real revenue and more risk to protect against.

5. Is coming up with an idea the same as starting a business?

No, they're two different steps. Coming up with and validating an idea tells you whether a problem is worth solving. Starting the business is everything that comes after: the plan, the legal basics, the first sale, and the systems that keep it running. It's possible to have a great validated idea and still not have a business yet. The business exists once you've put structure behind it and started operating.

P.S. If you're still deciding what to build, we've also put together a list of small business ideas for high school students, a rundown of ways to get a high school business education if you want more structured learning alongside doing the work, and a look at business programs for high schoolers if you're ready for more hands-on support.